Pinion Blog

MOIC vs. TVPI: What They Measure, Why They Differ, and How to Read Them

MOIC and TVPI are often used interchangeably, but they answer slightly different questions. This piece explains what each metric measures, when to use which, and how to read the patterns they reveal in your portfolio.

Two of the most common metrics in private investing are MOIC and TVPI. They're often quoted in the same breath, and on a casual read they seem to mean roughly the same thing — both are ratios, both tell you how much your investment has grown, both get bigger when things go well. In a lot of conversations, people use them interchangeably.

This seems like a safe place to share: I thought MOIC and TVPI were essentially the same until recently.

They aren't interchangeable. They answer slightly different questions, they're calculated differently, and the gap between them can tell you something useful about your portfolio. If you're tracking direct angel investments, fund commitments, or both — which is the world Pinion was built for — getting clear on what each one is actually saying is worth a few minutes.

This piece walks through what each metric measures, how they differ, when to use which, and how to read what they're telling you about your book.

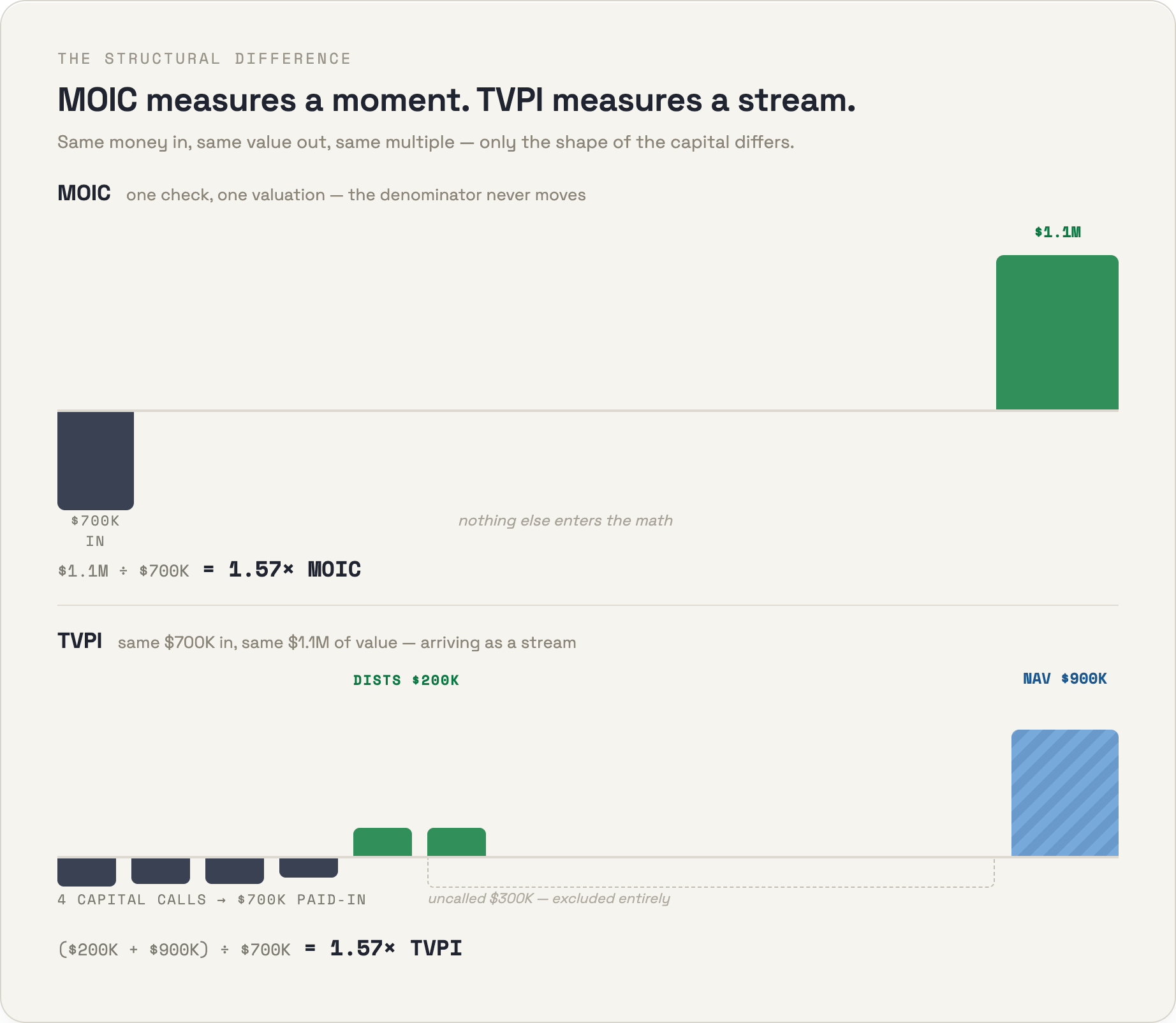

What MOIC measures

MOIC stands for Multiple on Invested Capital. It's the simplest possible expression of investment performance: how much is your money worth now, relative to how much you put in?

The formula is:

MOIC = Current Value ÷ Invested Capital

If you wrote a $100K check into a startup and that stake is now worth $300K on paper, your MOIC is 3.0x. If the company exited and you got $500K in cash, your MOIC is 5.0x. If the company went sideways and the stake is now worth $40K, your MOIC is 0.4x.

That's the whole metric. It doesn't matter whether the value is realized (cash in your pocket) or unrealized (a paper markup based on the latest round). It doesn't matter how long it took. It doesn't matter whether you got there in a straight line or through three down rounds and a recap. MOIC just asks: for every dollar I put in, how many dollars do I have now, on paper or in cash?

That simplicity is its strength. MOIC is easy to calculate, easy to explain, and easy to compare across deals. When you're sizing up a single investment — was this a good check? — MOIC gives you the cleanest possible answer.

What TVPI measures

TVPI stands for Total Value to Paid-In capital. It's a close cousin of MOIC, and the formula looks almost identical:

TVPI = (Distributions + Net Asset Value) ÷ Paid-In Capital

The structural difference is what counts as the numerator and denominator. TVPI is the standard performance metric in the institutional fund world, where the lifecycle of capital is more complicated than "I wrote a check, now I'm waiting." A fund draws down committed capital over time through capital calls, sends back proceeds through distributions, and holds the rest at NAV (net asset value) on its balance sheet. TVPI captures all three:

- Distributions (DPI piece): cash that's already been returned to LPs

- Net Asset Value (RVPI piece): the current carrying value of unrealized positions

- Paid-In Capital: the total capital that has actually been called and contributed (not the full commitment)

So if you committed $1M to a venture fund, $700K has been called so far, the fund has distributed $200K back to you, and your remaining stake is marked at $900K, your TVPI is ($200K + $900K) ÷ $700K = 1.57x.

The reason TVPI exists as its own metric is that, in fund investing, "invested capital" isn't a single moment — it's a stream. TVPI normalizes performance against the capital that's actually working, not the total you promised.

How they actually differ

For a single direct investment — one check, one company, one outcome — MOIC and TVPI are functionally the same number. If you wrote $100K and the stake is worth $300K, both metrics give you 3.0x. The distinction doesn't really show up at the deal level.

The differences emerge in three places:

1. Funds vs. direct deals. TVPI is the native language of fund performance because funds have called and uncalled capital, distributions, and NAV all moving at once. MOIC is the native language of direct deals because direct deals are simpler — you put money in, you watch the value change, eventually you get money back. When a fund manager talks about their track record, they'll quote TVPI (alongside DPI and IRR). When an angel talks about a specific deal, they'll quote MOIC.

2. Distributions and NAV split out. TVPI is often broken into its two components: DPI (Distributions to Paid-In, the cash you've actually received) and RVPI (Residual Value to Paid-In, the paper value of what's still in the ground). TVPI = DPI + RVPI. This split matters a lot — a 2.0x TVPI made up of 1.8x DPI and 0.2x RVPI is a very different beast than a 2.0x TVPI made up of 0.1x DPI and 1.9x RVPI. The first is mostly realized; the second is almost entirely on paper. MOIC doesn't natively make that split, though good portfolio tools (Pinion included) will track realized vs. unrealized separately so you can see the same picture.

3. Treatment of uncalled capital. TVPI ignores capital you've committed but haven't yet contributed. That's correct from a performance standpoint — uncalled capital isn't earning anything yet, so it shouldn't drag down or boost the multiple. But it means TVPI alone doesn't tell you about your commitment exposure. If you've committed $5M to a fund and only $1M has been called, your TVPI tells you how the $1M is doing, not what your full $5M position might look like when fully deployed. That's a separate question, and it's why fund investors look at TVPI alongside pacing data, not in isolation.

What neither metric captures, by design, is time. A 3.0x in three years is wildly different from a 3.0x in twelve years, but both have the same MOIC and the same TVPI. That's why both metrics are almost always paired with IRR (Internal Rate of Return), which is the time-weighted version. MOIC and TVPI tell you how much; IRR tells you how fast. You want all of them.

When to use which

For Pinion users — who typically hold a mix of direct angel investments and fund commitments — the practical rule is:

- Use MOIC when looking at direct investments. It's the right metric for individual checks. How is my Acme Corp position doing? 4.2x MOIC. Clean, comparable, intuitive.

- Use TVPI when looking at fund commitments. It's the right metric for fund vehicles, where called capital, distributions, and NAV all need to be in the same number. How is my Andreessen Fund VIII commitment doing? 1.7x TVPI.

- Use both, side-by-side, at the portfolio level. A blended portfolio of direct deals and funds is most honestly described with both metrics visible. Pinion's portfolio summary surfaces TVPI across all holdings (treating direct deals as fully called) so you have a single comparable number, while still letting you drill into MOIC at the individual investment level.

- Always pair with DPI and IRR. A multiple without a time dimension is half a story, and a multiple without a realized/unrealized split can be misleading. The dashboard is built to show these together for that reason.

What the numbers are telling you

This is the part most write-ups skip. A multiple is just a number — what matters is what the number implies about the underlying portfolio. Some general patterns worth knowing:

MOIC or TVPI under 1.0x. You're underwater. Total value is less than what you put in. For a young direct deal this is often noise — early markdowns, dilution from a flat round, normal lumpiness. For a fund three or more years in, it's worth attention. For a fund seven or more years in with low DPI and a TVPI under 1.0x, it's probably telling you the vintage didn't work.

MOIC or TVPI between 1.0x and 1.5x. Capital preserved, modest gain. For early-stage venture this is below expectations — the asset class only works if winners pay for losers, so a portfolio averaging 1.2x typically means the winners weren't big enough. For later-stage or growth investments, this can be a perfectly reasonable outcome depending on duration.

MOIC or TVPI between 1.5x and 3.0x. Solid territory. A fund finishing its life around 2.0x net TVPI is a good fund. A direct deal exiting at 2.5x is a respectable outcome. The IRR matters a lot here — a 2.0x in four years is very different from a 2.0x in ten.

MOIC or TVPI above 3.0x. Strong outcome. For direct angel deals, this is the territory where a single position starts meaningfully moving the whole portfolio. For funds, top-quartile vintages often land here. Worth noting: above 3.0x, the unrealized portion gets increasingly speculative — paper markups at 5x or 10x can compress dramatically by the time they realize.

A high TVPI with low DPI. This is the most important pattern to recognize. A fund showing 2.5x TVPI but only 0.3x DPI is telling you the gains are almost entirely unrealized. That doesn't mean they're fake, but it does mean they're vulnerable to revaluation, market conditions at exit, and time. The cash hasn't actually come back yet. The closer TVPI and DPI converge, the more "real" the multiple is.

A low TVPI with high DPI. Less common, but it happens — a fund that returned capital aggressively early and is winding down with little NAV left. The multiple may not look exciting, but the cash has been returned and the IRR is often strong because distributions came early.

Diverging MOIC across direct deals. When you scan your direct investments and see a wide spread — 0.2x, 0.5x, 1.0x, 1.0x, 1.0x, 1.0x, 8.0x — that's the venture power law showing up in your own book. It's the expected shape, not a problem. The question to ask isn't “why are so many at 1.0x?” but “do I have enough shots to catch a tail outcome?” Time also really matters here. Our portfolio is relatively young and 80% of our investments are sitting at 1.0x.

The metrics aren't the answer. They're the start of the conversation. What Pinion is built to do is give you that starting point — clear, current, and consistent across your direct deals and funds — so you can spend your time on the actual question: what does this tell me about my portfolio, and what should I do next?

If keeping track of your MOIC, TVPI, DPI, and IRR across direct deals and fund investments feels like more spreadsheet work than insight, Pinion can help.